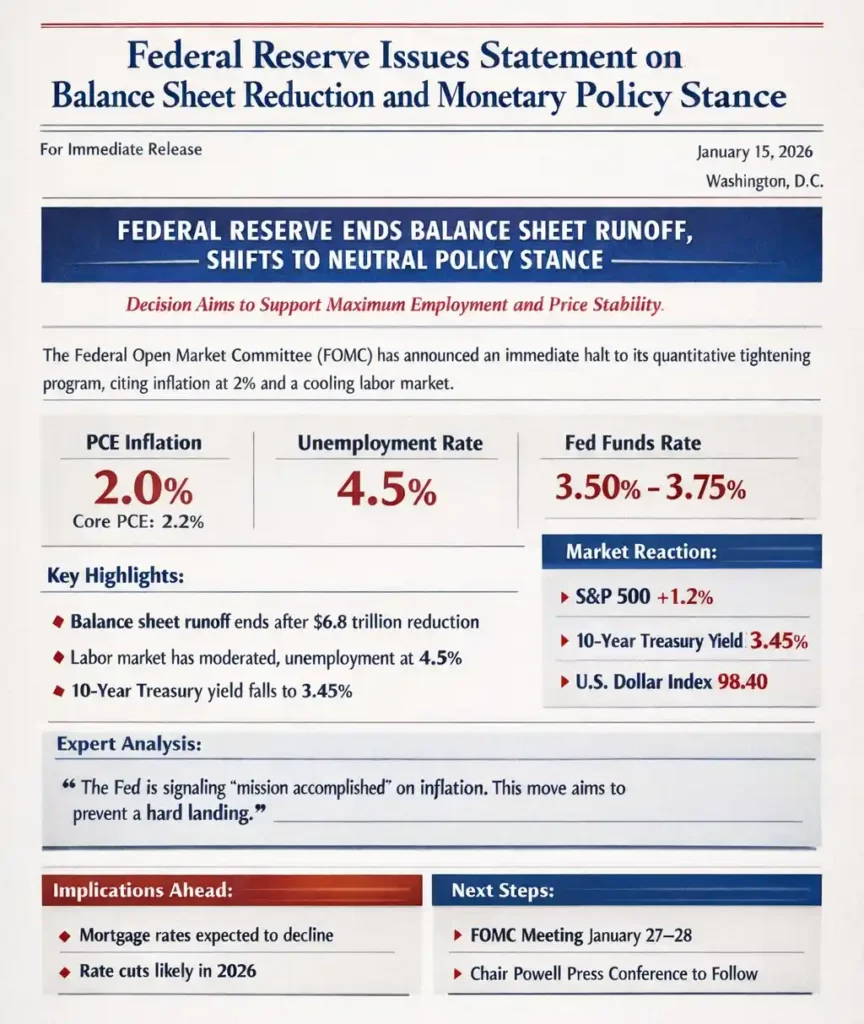

The Federal Open Market Committee (FOMC) today announced a decisive shift in its monetary policy implementation, signaling the conclusion of its balance sheet runoff program, commonly referred to as quantitative tightening (QT). The decision follows recent economic data indicating that inflation has stabilized at the Committee’s 2 percent objective, while labor market conditions have cooled toward more sustainable levels.

Transition to a Neutral Policy Stance

In a special directive issued ahead of the scheduled January 27–28 FOMC meeting, the Committee announced it will cease the decline of its securities holdings effective immediately, bringing an end to the monthly runoff caps that have been in place since 2022.

The Committee noted that reserve balances in the banking system are approaching levels consistent with the Federal Reserve’s ample reserves framework, and that continued balance sheet reductions could introduce unnecessary volatility in short-term funding markets.

“The Committee judges that the risks to achieving its employment and inflation goals are now roughly balanced,” the statement read. “With the Personal Consumption Expenditures (PCE) price index stabilizing at 2.0 percent and the unemployment rate edging up to 4.5 percent, the Committee is transitioning toward a neutral policy stance to support maximum employment while maintaining price stability.”

Key Economic Data Informing the Decision

Inflation:

The 12-month change in the PCE price index—the Federal Reserve’s preferred inflation gauge—registered 2.0 percent, down from 2.4 percent in late 2025. Core PCE inflation, which excludes food and energy, stands at 2.2 percent, its lowest level in five years.

Labor Market:

The unemployment rate has risen to 4.5 percent, up from 4.2 percent six months ago. Payroll growth has moderated to an average of 115,000 jobs per month over the past quarter, signaling a cooling but resilient labor market.

Interest Rates:

The target range for the federal funds rate remains 3.50 to 3.75 percent, following a 25 basis point reduction implemented in December 2025.

Background on Quantitative Tightening (QT)

Quantitative tightening has been a central tool in the Federal Reserve’s effort to withdraw excess liquidity from the financial system following the inflation surge of the early 2020s. By allowing Treasury securities and agency mortgage-backed securities (MBS) to mature without reinvestment, the Federal Reserve reduced its balance sheet from a peak of nearly $9 trillion to approximately $6.8 trillion.

Ending QT marks a significant policy pivot. While changes to the federal funds rate affect the price of credit, balance sheet policy influences the quantity of reserves and highly liquid assets available to the banking system. The decision is widely viewed as a safeguard to ensure sufficient liquidity in repo and funding markets, and to prevent a recurrence of the funding stresses experienced in late 2019.

Market Reaction: Stocks Rise, Yields Fall

Financial markets responded swiftly to the announcement, interpreting the halt of QT as supportive of global liquidity conditions.

- Equities:

The S&P 500 rose 1.2 percent to 6,485.50, led by interest-rate-sensitive sectors such as utilities and real estate. The Nasdaq Composite gained 1.5 percent. - Bonds:

The yield on the 10-year U.S. Treasury note declined 12 basis points to 3.45 percent, as investors revised expectations for long-term interest rates. - Currencies:

The U.S. Dollar Index (DXY) eased to 98.40, reflecting a reduced yield advantage as policy expectations turned more accommodative.

Expert Commentary and Economic Outlook

Dr. Sarah Collins, Chief Economist at Global Macro Analytics, commented:

“The Federal Reserve is effectively declaring ‘mission accomplished’ on inflation. By halting balance sheet runoff now, policymakers are buying insurance against a recession. With the labor market cooling, the Fed is acting preemptively to avoid a hard landing.”

The move aligns with projections from the December 2025 Summary of Economic Projections (SEP), in which the median participant forecasted trend growth of 1.8 percent in 2026. The timing—two weeks ahead of the scheduled FOMC meeting—suggests heightened sensitivity to liquidity conditions.

Implications for Borrowers and Investors

Mortgage Rates

With the Federal Reserve no longer reducing its MBS holdings, supply pressures in the mortgage bond market are expected to ease. This could narrow the spread between Treasury yields and mortgage rates. As a result, the 30-year fixed mortgage rate, currently near 5.8 percent, may decline further, supporting housing activity ahead of the spring season.

Inflation Outlook

While headline inflation has returned to the 2 percent objective, the Committee emphasized it remains “highly attentive to inflation risks.” The emergency phase of inflation-fighting policy has concluded, but a return to near-zero rates is unlikely absent a severe economic downturn.

Interest Rate Path

Interest rate futures now reflect a 75 percent probability of an additional 25 basis point cut at the January 27–28 meeting. The December “dot plot” suggested the federal funds rate could settle near 3.0 percent by the end of 2026. The end of QT reinforces this more accommodative outlook.

Savings and Deposits

As policy moves toward neutrality, yields on high-yield savings accounts and certificates of deposit are expected to decline. The peak deposit rates exceeding 5 percent in 2024 and 2025 are likely behind us, prompting savers to consider locking in current yields or shifting toward intermediate-term bonds.

Global Implications

The Federal Reserve’s pivot provides added flexibility for other major central banks. The European Central Bank and the Bank of England, both facing slowing growth, may find greater room to ease policy without triggering sharp currency depreciation. Emerging markets stand to benefit from improved global financial conditions and a softer dollar, easing pressure from dollar-denominated debt.

Conclusion

Today’s announcement marks the definitive conclusion of the post-pandemic tightening cycle. With inflation and employment risks now in balance, the Federal Reserve has signaled that its dual mandate objectives are once again aligned. As balance sheet runoff ends, policy focus shifts squarely to sustaining a soft landing—an outcome that appears increasingly attainable. Markets will now look to Chair Powell’s press conference on January 28 for further guidance on the trajectory of interest rates through the remainder of 2026.